Your Deposits Aren't Leaving. Your Governance Already Has.

The second deposit problem and why your dashboard won't show it

This post was inspired by Ron Shevlin’s recent piece on deposit displacement, which nails the visible part of the story. The $3.15 trillion that left banks for fintech accounts between 2020 and 2025 is real. The paycheck motel argument holds.

But there’s a second problem sitting underneath that one, and nothing in standard reporting picks it up.

Deposits don’t have to leave to become unstable.

The bank that looked fine

Earlier this year, I published on SSRN a composite regional bank in the Asia Pacific, patterns drawn from real observed data. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=6147568

On the metrics, this bank was fine. LCR comfortable. NSFR above minimum. Deposit balances holding flat. No run, no regulatory concerns, credit book clean.

And yet the SME and corporate operating accounts were changing. Not because clients were under pressure - they weren’t. Rates had moved, and money market funds were offering 100–150 basis points more than the bank’s operating accounts. The treasury software was doing the rest: idle balances swept out each night above a set threshold, back in by morning to cover the day’s payments. No call to the relationship manager. Just a rule, running on a schedule nobody at the bank had written.

Screen balance: flat. The money itself is gone by 6 pm, back by 8 am.

The analogy that fits - a tenant paying rent every month on time, but who quietly sublet the flat six months ago and only comes by to collect the post. Dashboard says occupied. The flat’s been empty most nights.

What that flat balance was hiding

The loans were still on the books. Still needed funding. But the deposit money the bank assumed was backing them, not reliably there anymore after the close of business. So, wholesale markets filled the gap. Interbank borrowing, institutional money, all of it priced higher. Wholesale funding costs moved from roughly 3.6% to above 4.4% inside two quarters.

Loan book: unchanged. Liability mix: quietly not what it was.

LCR stayed green. NSFR stayed green. No alarm.

Funding quality had deteriorated - not from deposits leaving but from the deposits that stayed, stopping from behaving like stable funding. That distinction matters. Most governance frameworks weren’t designed to see it.

Why nobody caught it

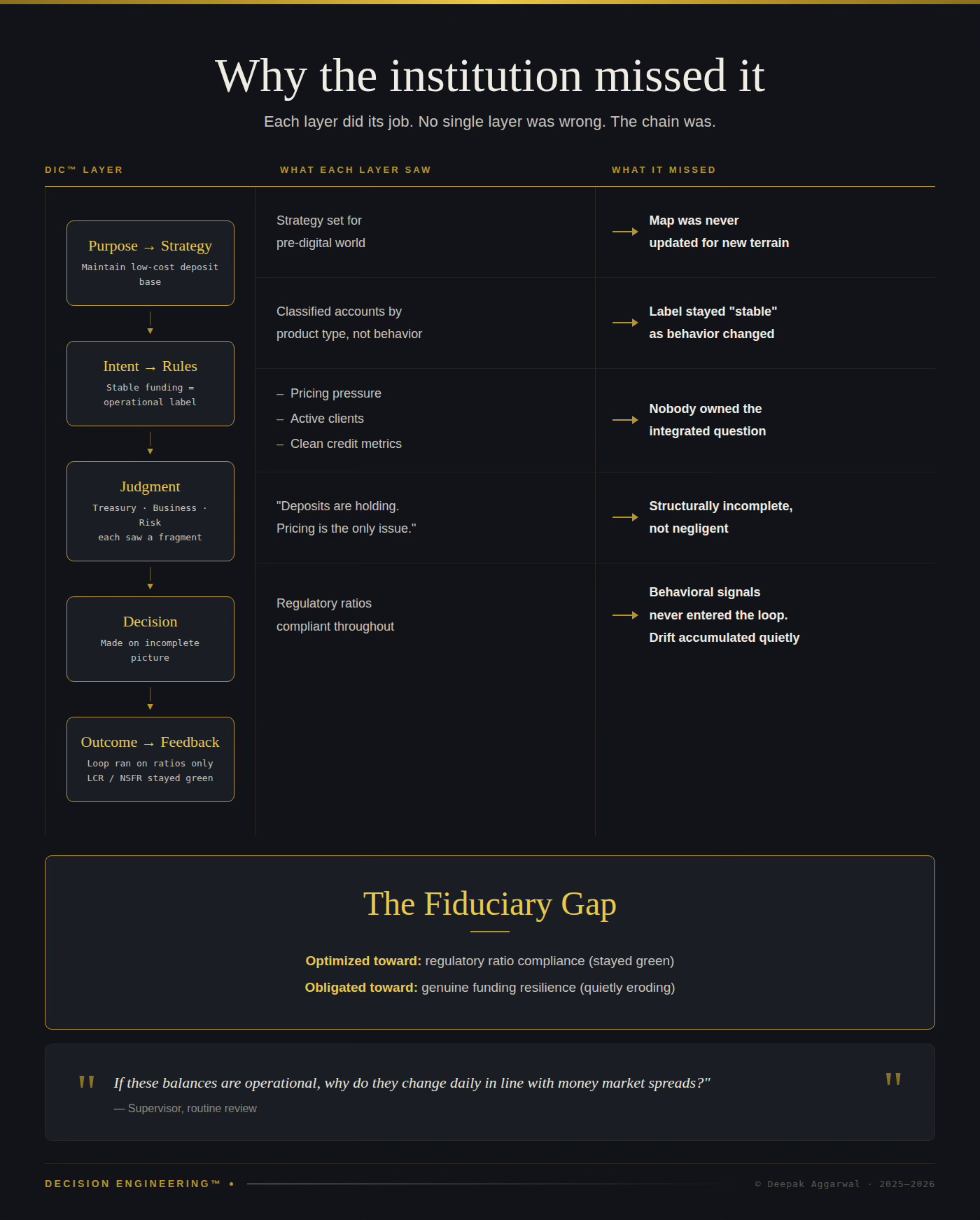

Not a failure of any single team. A chain failure.

The strategy had been built for a deposit base where money moved when a client decided to move it - a deliberate act, visible, slow enough to manage. That deposit base no longer existed. Treasury platforms with API connectivity and automated sweep logic had changed how corporate and SME liquidity was managed, and the strategy had never been updated to reflect any of it.

Rules classified SME operating accounts as stable funding. Product label: operational account. Nobody had formally checked whether the behavior still matched that label. It didn’t.

Across the functions, the individual reads were accurate. Treasury saw a pricing competition problem. Business lines saw active, transacting clients. Risk saw clean credit. What none of them owned and what the architecture didn’t require anyone to own - was the question underneath all three: Is the funding base actually behaving the way the models say it is?

It wasn’t. But asking that question wasn’t anyone’s job.

The feedback loop ran on LCR and NSFR. Both compliant. Behavioral signals - sweep velocity, rate sensitivity, effective duration compression in the SME book - never entered the formal governance cycle. Drift had been accumulating for quarters before a supervisor named it.

Every layer functioned as designed. That was precisely the problem.

The Fiduciary Gap

There’s a name for this kind of structural divergence: the Fiduciary Gap.

The institution was optimized toward regulatory ratio compliance. Its actual obligation was something different - sustainable funding, money that would genuinely be there when the loans it backed needed servicing. For years, those two things aligned. Then, without anyone deciding it, they stopped.

No rule broken. No individual decision wrong. Ratios green while the behavioral reality underneath shifted quarter by quarter.

It surfaced in a routine supervisory review. One question from across the table:

“If these balances are operational, why do they change daily in line with money market spreads?”

Quiet room. No violation to point at. No clean answer either.

That’s what the Fiduciary Gap looks like when it surfaces - an institution that had been reporting stability it hadn’t verified, not dishonestly, but because the assumption had never been formally re-examined. The old definition of stable funding had stopped being accurate some time ago. The governance architecture hadn’t noticed.

If you’re inside a bank reading this

One question worth sitting with: do your deposit stability numbers reflect how clients actually manage liquidity in 2026, or how they managed it before treasury platforms could connect to bank accounts via API and sweep balances on a nightly rule?

Not the LCR. The behavior behind it.

Are your SME and corporate clients running automated sweeps you don’t see? Can your treasury team tell the difference between a balance that’s genuinely sticky and one that’s clearing payments in the morning and sitting in a money market fund by evening? Is that distinction in your stability modelling at all?

If those answers aren’t in the data, that is the finding.

The retail displacement story Ron documented is visible. Bankers know it. The behavioral reclassification of SME and corporate operating balances is the one that doesn’t surface in outflow reports - it surfaces in funding costs, in NIM compression, in wholesale dependency, typically a year or more after the behavior causing it started running.

Boards that identify this early get to make a deliberate strategic call - which balances to defend, at what pricing cost, with what funding trade-offs. The ones that find out from a regulator in a quarterly review don’t get that conversation first.

Stability isn’t a classification decision made at account opening. It’s something that has to be re-earned continuously, against actual observed behavior - not assumptions that made sense a decade ago.

This post draws on my January 2026 SSRN paper “When Stable Deposits Stop Being Stable: A Behavioral Reassessment of Core Funding in Regional Banking.” The Fiduciary Gap and Decision Integrity Chain™ are proprietary components of the Decision Engineering™ framework.

© Deepak Aggarwal, 2025–2026. All rights reserved.

One of the challenges this exposes is the obsession with individual accountability. Effective systems are about collective responsibility, not attributing blame.