The Distributed Decision Network

How retail banks became nodes — and lost control of their own decisions

The boundary is gone. Not weakening. Not slowly dissolving while everyone wrote white papers about it.

Gone.

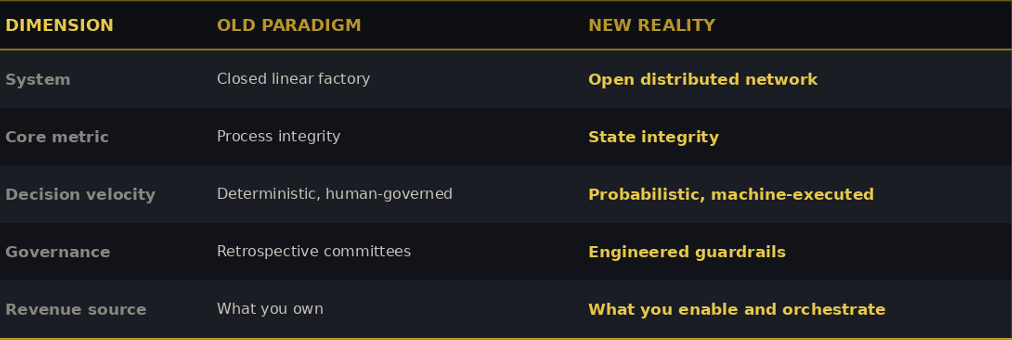

For decades, banks ran as closed systems. Products, risk, servicing, controls - all inside the same corporate wall. Digital transformation meant digitizing the factory. AI meant making the factory faster.

That model is dead.

Today, a single retail banking transaction — one tap, one millisecond — touches technology the bank doesn’t own, data it didn’t collect, models it didn’t build, and infrastructure it doesn’t control. All of it simultaneously. Before any human sees it.

The bank is no longer an institution. It is a node.

Four Shifts Nobody Governed

My earlier research identified four structural forces remaking the institution. (Full analysis: Reimagining the Future of Banking in a Protocol-Driven World). Each has accelerated. None has been adequately governed.

Banks used to compete on proprietary infrastructure - their own rails, their own platforms, their own closed systems. That model is under pressure. Value is beginning to flow across shared infrastructure that nobody owns exclusively. UPI. Onyx. Open finance networks. The banks still defending closed platforms risk fighting for territory that may no longer determine who wins.

Compliance is starting to look different in the institutions paying attention. The direction of travel is clear - rules embedded into the decision itself before it executes, not reviewed after the fact. A handful of banks are moving that way. Most are still producing policy documents that nobody operationalises.

ESG scoring has a credibility problem that greenwashing created faster than any regulator could address. What needs to replace it is harder to fake - ethics built directly into how products are priced and structured. Carbon-aware lending. Dynamic ESG-linked products. Real-time monitoring rather than quarterly reporting. The architecture exists. The adoption doesn’t yet.

Identity is shifting from a compliance file to something more valuable — a trust asset that can be managed and brokered on behalf of the customer. Federated identity, reusable credentials, consent-led models. The banks that move early on this will own a relationship layer that goes well beyond deposits and loans. Most are still treating it as a KYC requirement.

The Unbundling Nobody Governed

Fintech broke the bank apart. Products, channels, data, risk — what used to sit inside one institution now sits across dozens of partners, platforms, and providers.

Then AI arrived and started making decisions across all of it. Fast. Autonomously. At a scale no human oversight structure was designed to handle.

The governance never kept up.

Old-style governance was built for a closed system - clear hierarchy, defined handoffs, someone in the room when the decision was made. That model doesn’t work when the decision is made in milliseconds across systems the bank doesn’t fully own or control.

It doesn’t slow down and adapt.

It just stops working.

Where Does Accountability Live?

Think about what happens when a bank’s automated system makes a bad call. The data came from outside. The model was built by a vendor. The decision executed inside the bank’s own systems. Something went wrong somewhere in that chain.

Who is responsible?

Not the policy document. Not the risk committee that meets monthly. Not the compliance deck that got signed off last quarter.

Most institutions are missing the core distinction. Ownership is structural. Accountability is cultural. But one cannot exist without the other, and in a distributed decision network, most banks have neither.

When decisions are made across multiple systems, vendors, and data sources, nobody automatically owns what happens. Ownership has to be deliberately designed into the architecture. In most institutions, it isn’t. So accountability - which can only form where ownership already exists - never had anywhere to land. That is the design gap. Not a culture problem. Not a leadership problem. A decision architecture problem.

This is what Decision Engineering™ is built to solve. The Decision Integrity Chain™ builds ownership into the system before decisions are made — not after something goes wrong. Because you cannot hold people accountable for outcomes in a system that was never designed to assign responsibility in the first place.

Banks are deploying AI into that unowned space. That gap is where the failures are accumulating.

This stopped being a technology problem some time ago. The question now sitting on every leadership table, whether they’ve named it or not, is simple: Is our institution designed to own its decisions, or are we just hoping accountability works itself out?

The danger was never the fintechs. It was always irrelevance. And the reward was never market share. It is trust-share.

The institutions that see this now will architect for it. The ones that don’t will regulate their way through the wreckage.

When regulatory compliance buckles inside a distributed decision network — does it fail at the protocol layer, or does it fail because governance was never engineered in to begin with?

© Deepak Aggarwal, 2026. All rights reserved. Decision Engineering™ is a trademark of Deepak Aggarwal. Reproduction or use without written permission is prohibited.